Growth and internationalisation of Italian companies

The Italian production ecosystem is characterised by large, sector-leading companies with an international footprint, as well as by a strong presence of medium-sized companies, often highly specialised in specific sub-sectors and deeply rooted in their local territories. These features provide both agility and niche capabilities, but they also set limits in terms of resources for large-scale international investments: therefore, many companies need to bridge the gaps in managerial, financial, and digital skills in order to address increasingly complex and highly innovative markets1.

In a global context marked by technological transitions, geopolitical tensions, changes in consumption patterns, and new sustainability demands, both growth and internationalisation represent two key drivers for strengthening the competitiveness of “Made in Italy". This scenario has prompted, and continues to prompt, companies to redefine their business models and rethink their strategies.

MACRO-TRENDS FOR THE COMPETITIVENESS OF MADE IN ITALY

As of today, four main macro-trends are reshaping the competitive landscape within which Italian companies operate:

- Digitalisation & Automation: the rise of new technologies is revolutionising industry, accelerating production efficiency and opening new frontiers in innovation, from robotics to artificial intelligence

- Supply Chain Resilience & Diversification: growing geopolitical and climate instability is pushing companies to strengthen resilience and diversify supply chains, focusing on multiple suppliers, local production, and predictive technologies to reduce risks and ensure operational continuity

- Reshoring & Nearshoring: this phenomenon is gaining momentum in the industry, with more and more companies bringing production back to Europe or nearby areas to reduce dependence on faraway suppliers, improve responsiveness and strengthen the value chains’ stability

- Talent Development: talent development has become a strategic pillar for the industry, with increasing investments in continuous training, digital upskilling, and leadership programmes to attract, develop, and retain key skills in an increasingly competitive labour market.

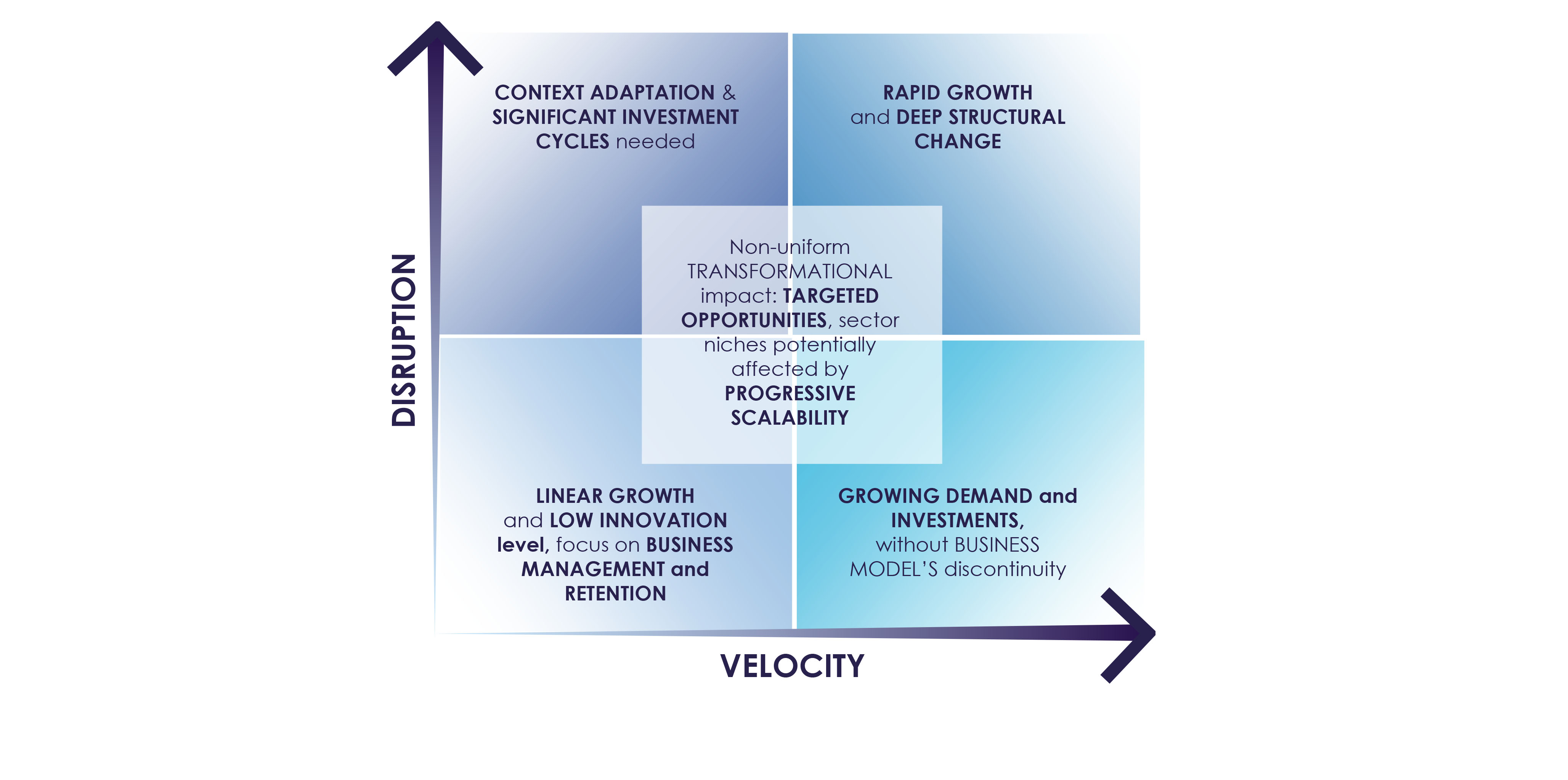

DISRUPTION AND VELOCITY: THE DIMENSIONS OF BUSINESS COMPLEXITY

In an environment characterised by high dynamism and uncertainty, the speed of change and the corresponding level of disruption can be identified as the main aspects of business complexity across different sectors; based on these variables, companies need to identify and implement industrial strategies that perfectly suit the competitive and industrial context in which they operate.

As a matter of fact, it is possible to identify “linear growth” strategies when the speed of change is relatively moderate and the impact of disruption is limited: these strategies are applicable to industrial manufacturers serving end markets such as transport -especially logistics- Telecommunications, and durable goods production. At the opposite extreme there are strategies involving a radical transformation of the business model, applied in sectors where the speed and impact of change are at their highest, such as Automotive, Aerospace & Defense, and the Tech and Energy sectors.

Between these extremes there are intermediate strategies and business models that adapt to the context of the various end markets in which companies operate.

THE MOST ACTIVE SECTORS IN M&A

External growth and international expansion can be key drivers in accelerating and reshaping the business models of industrial companies, enabling them to promptly seize development opportunities in traditional segments or in areas adjacent to those in which they already operate.

In this scenario, M&A, potentially combined with opening up the share capital, can become a key success factor allowing to remain competitive or to strengthen the leadership within the sector. As a matter of fact, in 2024, in Italy, within the “Industrial Market” 2, 369 deals were announced, while by the end of 2025, 336 transactions have been recorded, with a total value of approximately 7.8 billion euro3, despite the significant geopolitical and trade uncertainty experienced during the year. The “Industrial Market” sector is therefore confirmed as one of the most active in terms of M&A activity, accounting for approximately 24% of total transactions carried out in Italy in 2025 (26% in 2024).

TOWARDS NEW BUSINESS MODELS

As illustrated by the figures above, extraordinary finance strategies defined by companies will increasingly tend to focus on more selective and targeted transactions, aimed at optimising the product portfolio, consolidating revenue growth, and strengthening resilience in response to global market dynamics. In this context, companies are accelerating the implementation of strategic technologies such as Artificial Intelligence, reshaping their business models and focusing on initiatives able to generate sustainable long-term value.

Moreover, the softening of traditional boundaries between sub-sectors shows a progressive reorganisation of the industry around new growth trends, where creative and synergistic collaborations - both between companies and between companies and financial institutions (e.g., Investment Funds) - serve as concrete levers to create value, enhance competitiveness, and increase profitability4.

THE BANK IN SUPPORT OF CORPORATE STRATEGIES

In conclusion, the choice of a company’s growth strategy should be driven by a realistic assessment of the speed of change and of the level of disruption within the relevant sector: growing without losing identity, innovating without compromising financial sustainability, and turning opportunities into tangible value for clients and stakeholders are the key directions through which the Italian production ecosystem will be able to sustain its success on a global scale.

Thanks to its broad and well-established cross-functional expertise, as well as a wide range of tailor-made services and products, Intesa Sanpaolo's IMI Corporate & Investment Banking Division supports Italian companies across various industrial sectors, with the aim of enhancing competitiveness and fostering growth in an increasingly complex global market.

1 https://www.ice.it/it/sites/default/files/inline-files/RAPPORTO%20ICE%2025%20-%20web%20vers.pdf

2 Industrial Markets (IM) include, among others, construction, chemicals, and automotive, as well as typical industrial activities such as steel industry, mechanical engineering, and plant engineering

3 KPMG, "Il Mercato M&A 2025 e i principali trend (The 2025 M&A Market and the main trends)", AIFI conference, Milan, 26 January 2026

4 https://www.pwc.com/it/it/services/deals/trends/ma-industrials-services.html